Whether it involves crowding onto public transportation or white-knuckling it on a bumper-to-bumper freeway, few enjoy a long, urban commute to work. A new analysis of the cost of commuting in different U.S. cities by the U.S. Chamber of Commerce helps to quantify its effect on overall office demand.

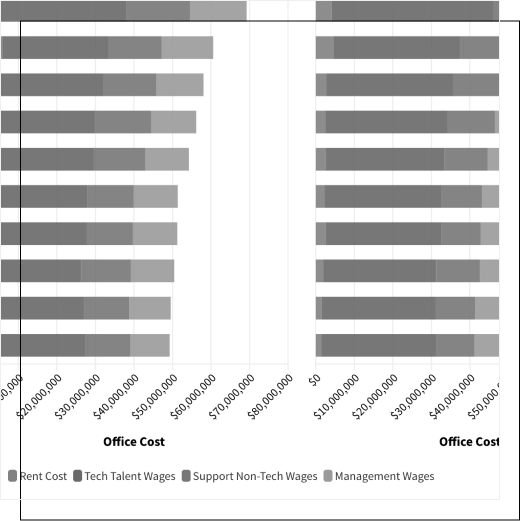

Using data from the U.S. Census Bureau’s American Community Survey, the Chamber of Commerce calculated the opportunity cost of commuting in more than 150 cities by multiplying the average hourly wage in each city by the average length of a round-trip commute for those who work there.

A further comparison with CoStar data on office availability in these cities shows that the amount of available office space has increased in most markets where the annual opportunity cost of commuting exceeds the national average of approximately $5,748. While in others the relationship between commuting and availability is weaker.

The overall amount of available office space in the U.S. has risen by more than a third since the end of 2019 as office tenants adjust to the needs of the post-pandemic workplace. The increase has been particularly pronounced in the urban cores of major markets, with commuting intuitively a likely factor. That link is now backed by data.

To explore this relationship more closely, CoStar calculated the change in available space since 2019 for every city with both office availability data and commuting cost data from the Chamber of Commerce’s study. Where feasible, availability data for the central business district or urban core of a city was used.

The results show a meaningful relationship, as markets with a higher cost of commuting tend to have a larger increase in the amount of available office space.

Moreover, several Western, tech-oriented markets such as San Francisco, Seattle and Sunnyvale at the center of Silicon Valley in California, rise to the top of the list in terms of both office availability and commute cost. On the other hand, several smaller metropolitan areas, along with others in the Sun Belt, have both a lower commute cost and a smaller increase — or even a decrease — in office availability. The implication is that office demand has held up more strongly in cities where commuting is shorter and less costly.

A notable number of Americans say they despise their commutes and suggest in surveys a variety of things, both serious and tongue-in-cheek, that they would rather do. Given the disdain for long commutes, it stands to reason that people would be more resistant to high-frequency attendance at downtown offices in cities with the costliest commutes. The corresponding impact on demand for office space is now evident, with commuting joining the list of risk factors affecting office market fundamentals.